7 Percent of US Startups Financed with Home Equity

Home equity is one place entrepreneurs find startup money, study shows. Let’s take a closer look at who is tapping home equity for startup money and the industries where it’s most common.

Entrepreneurs who need to find startup money may tap credit cards, use personal savings, hit up friends and family, court investors, team up with partners, crowd-fund – and – yes – leverage home equity to get their business off the ground. EyeOnHousing.com reports that about 1 in every 14 startups today are funded with money available to a homeowner in a home equity loan.

Which US Entrepreneurs Find Startup Money in Home Equity?

Women Entrepreneurs Find Startup Money in Home Equity More Often But…

Female entrepreneurs are slightly more likely to find startup money in home equity financing than men. 7.8 percent of female-owned startups were funded through homeowner equity vs. 6.6 percent of male-owned startups. However, when homeowners also had equal ownership in a startup, 10.8 percent chose to fund their new business through the money available to them in home equity.

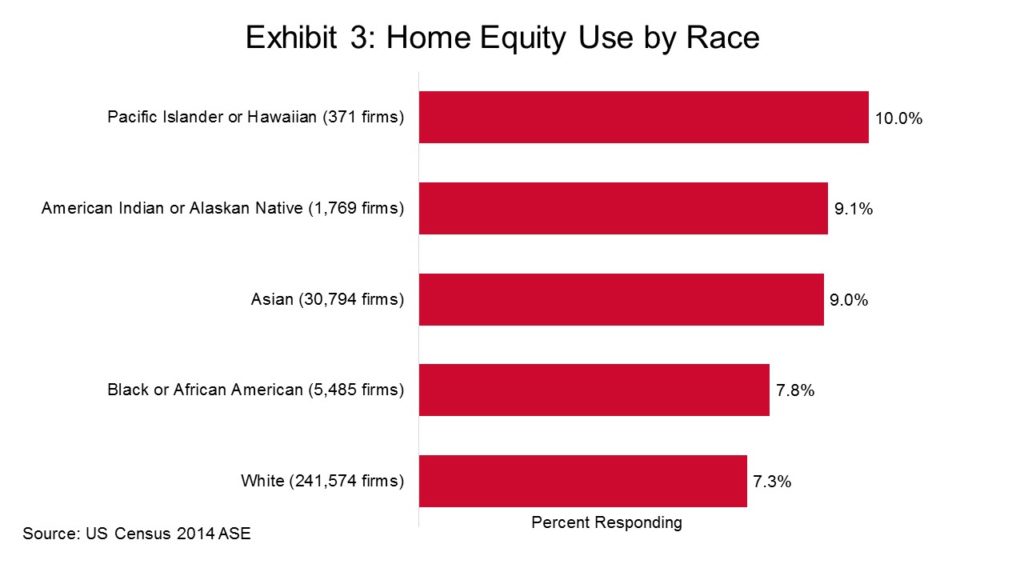

Home Equity Use by Race to Find Startup Money

According to 2014 US Census Bureau data, 10 percent of startups owned by Pacific Islanders or Hawaiians were funded through homeowner equity, representing 371 businesses. Here’s how the numbers break down in terms of home equity use by race:

- 371 Startups – Pacific Islander or Hawaiian – 10%

- 1,769 Startups – American Indian or Alaskan Native – 9.1%

- 30,794 Startups – Asian 9%

- 5,485 Startups – Black or African American – 7.8%

- 241,574 Startups – White 7.3%

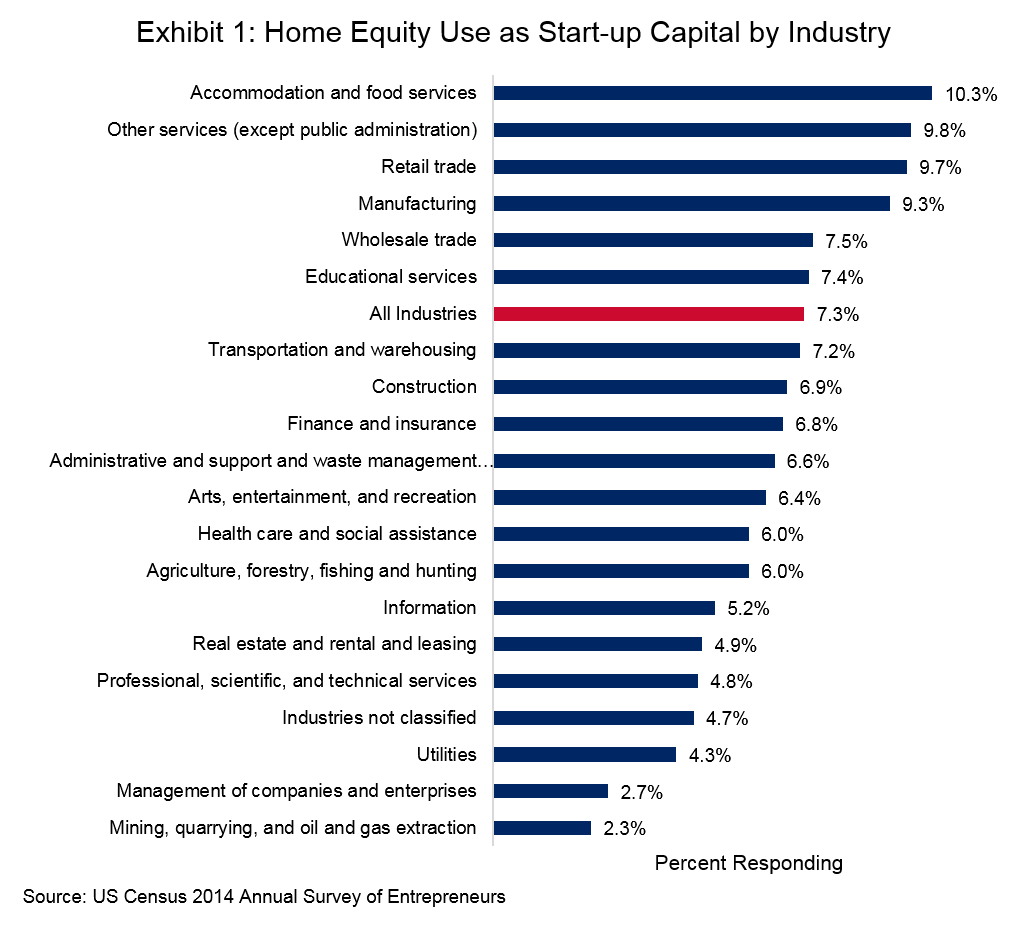

Where Entrepreneurs Find Startup Money by Industry

Accommodation and food services (which includes restaurants) is the industry where homeowners are most likely to leverage their homeowner’s equity for startup capital. More than 1 in 10 startups in this industry were funded with money available from home equity. Topping out the top five specific industries where homeowner equity was the source of startup capital are:

- 3% – Accommodation and food services

- 7% – Retail

- 35 – Manufacturing

- 5% – Wholesale trade

- 4% – Educational services

The five industries where home equity is least-used for starting a new business are:

- 3% – Mining, quarrying, oil and gas extraction (oilfield, natural gas and energy)

- 7% – Management of companies and enterprises

- 3% – Utilities

- 8% – Professional, scientific and technical services

- 9% – Real estate and rental and leasing

Using Home Equity to Finance a Business

If you’re a home owner, there are good reasons to meet with your mortgage agent every year, not just just when you’re in the process of buying a new home. To assess whether a home equity loan or line of credit is available to you in the first place, how much is available, and whether it’s advisable for you to leverage home equity to finance your business or some other project.

An Entrepreneur.com article lists some of the questions you should consider as a homeowner before leveraging the value you have in your house for business purposes. These would be great questions for you to talk over with your mortgage lender and your financial adviser, such as your tax or investment expert:

- Is the potential return on investment greater than the cost – not just payments but interest over time

- Is the home equity loan rate adjustable or fixed – would an interest rate hike make this financing much more expensive

- Is your home appreciating – will it continue to increase in value or is there a chance that taking a home equity loan now along with anticipated depreciation put you under water

- How will this affect your taxes – you might not be able to deduct the interest from taxes since the equity isn’t being reinvested in the home

- Do you need to preserve home equity for borrowing power in the future

- Can you recoup the money quickly from your business if needed – how liquid is your business

- Do you have a lot of other debt – and will your other debt affect your interest rate

- Do you have the cash flow to repay the loan – even if the business doesn’t pan out

If you decide that home equity is the appropriate way to fund your startup, you might also consider a home equity line of credit (rather than a home equity loan). For instance, using a home equity line of credit (HELOC) offers a more flexible option; if you don’t need to use the whole amount, you can borrow from your home’s equity more conservatively, taking only what you need when it’s truly needed. On the other hand, a HELOC’s interest rate is variable, so you may end up paying more for this type of financing.

Another reason you might choose to find startup money in your home’s equity is the interest rate and speed of funding available compared to many other types of financing. Home equity loans can usually be processed more quickly than bank business loans, since they are based on independently-appraised collateral and mortgage lenders don’t have to consider whether your business startup is going to pay off. Home equity loan rates are also usually lower than bank business loans (for the same reason) and will probably be significantly lower than the rates you would pay to finance your startup using credit cards.

You might also like: 5 Things to Do Before You Start a New Business [Infographic]

Leave a Reply

Want to join the discussion?Feel free to contribute!